Press Release

IBR - Covid-19 and the resilience of the private sector

30 Jul 2020

30 July 2020 - The Grant Thornton International Business Report for H1 2020, conducted globally in May and June, shows that 65% of mid-market businesses expect a fall in their 2020 revenues, with many adjusting future strategy incorporating more crisis management and remote working and additions to technology platforms to ensure continuity and improved flexibility. Many businesses are looking at supply chain with 1 in 4 set to make fundamental changes to their products and services.

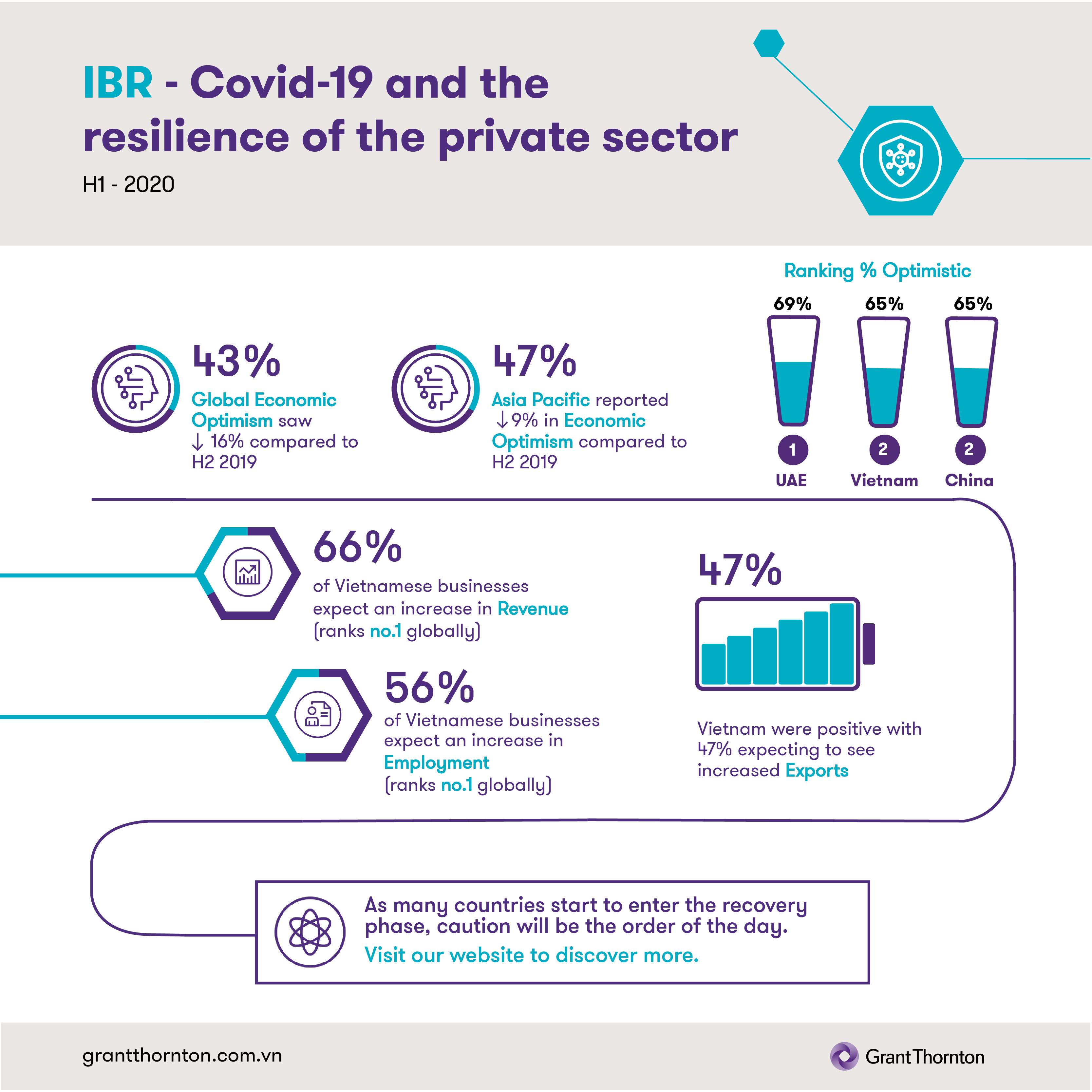

Globally, Economic Optimism declined 16 percentage points in comparison with H2-2019, with 44% of firms reporting a slight or very pessimistic outlook for their country’s economy over the next 12 months.

However, Asia Pacific reported a more optimistic outlook. Nearly half of all firms retained an optimistic outlook for the economy over the next 12 months. In contrast to trends seen in other regions, the decline in Optimism is relatively mild, falling by 9% (compared to the global average of 16%). Optimism in Vietnam ranked second globally together with China, 4% points behind the UAE with 65%, down from 82% in H2 2019. This may be due to timing of the survey—the pandemic peak in Asia was earlier and many economies have proven more successful in containing the outbreak.

Only 34% of firms globally are expecting an increase in Revenues in the next 12 months, down from 54% in H2-2019 and comfortably a survey-record low (beginning Q2-2011). The outlook for Profitability is similar with only 32% of firms expecting an increase, also a series low. Asia Pacific was similar in expectations with 35% of firms expecting an increase in revenues down from 59% in H2 2019, however Vietnam ranked no.1 globally with 66% of respondents expecting an increase in revenue but down from 93% in H1 2019.

This decline in revenue and profit expectations, globally, signifies a potentially difficult period ahead for many companies, as hopefully the global economy emerges from lockdown.

The current environment has driven a large spike in Economic Uncertainty. 66% of firms identify uncertainty as a business constraint (with nearly 1-in-3 firms identifying it as a major constraint). This was similar to Asia Pacific at 65% (H1 2019 50%) however Vietnam was more optimistic with 54% of firms believing it was a constraint compared to 47% in H2 2019.

The weaker outlook for business performance (revenues and profits) is likely underpinned by a number of key factors:

- Fewer firms globally expect to increase Selling Prices (32% down from 41%), in line with weaker inflation dynamics, which is underpinned by the sharp collapse in demand and falling energy prices. However, firms in Vietnam were more optimistic with 42% expecting higher selling prices.

- External demand is weakening as reflected by a decline in firms expecting an increase in Exports (25%, down 11 percentage points), although it remains much higher than previous series lows) whereas firms in Vietnam were again much more positive with 47% expecting to see increased exports, in the coming 12 months down from 75% in H2 2019.

- 55% of firms identify a Shortage of Orders as a constraint to business, with nearly 1-in-4 firms identifying it as a major constraint. Vietnam had a similar response as did all firms in Asia Pacific.

The collapse in demand, elevated levels of uncertainty, and concerns over a finance availability will all contribute to a decline in Investment intensions. This decline is most evident across capacity investments intentions (i.e., new buildings, plant & machinery) than across R&D, tech, and staff investment intensions. However, yet again Vietnamese companies proved more optimistic 53% planning to increase investments into Plant and Machinery, 50% into new buildings and 58% into R&D. Much higher than Asia Pacific which showed 28%, 23% and 40% respectively. This could well reflect the movement of manufacturing away from China into Vietnam and expectations of opportunity arising from the ratification and coming into force of the EU Vietnam Free Trade Agreement.

The Covid-19 pandemic has underpinned a huge labour market shake-out and less than 30% of firms anticipate hiring new staff in the next 12 months, down from nearly one-half in H2-2019. However, whilst this was consistent with Asia Pacific, more than 50% of firms in Vietnam expected an increase in labour, however this may be due to the fact that more people were laid off in Vietnam as the pandemic hit earlier than many countries.

Travel & Tourism and Transport were globally the worst hit sectors with optimism being recorded at 33% and 32% respectively and accordingly they are expected to suffer a significant negative and lasting shock—reflected in the survey with over 82% and 68% of firms in Tourism and Transportation respectively anticipating a decline in revenues this year as a consequence of Covid-19

As many countries start to enter the recovery phase, caution will be the order of the day. Businesses can be more vulnerable so a continual focus on cash flow, people, safety and the prioritisation of resources will be critical.

For further information, please contact:

Ms Ngo Thi Kim Van

Senior Manager

Marketing and Communications

E van.ngo@vn.gt.com

M +84 909 044 214