Strengthening representation where decisions are made

Women in Business 2026

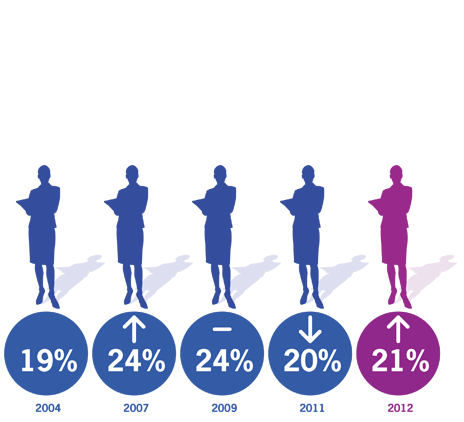

Vietnam continues to outperform global averages in women’s leadership. Explore key insights from Grant Thornton’s Women in Business 2026 report on gender diversity and CEO representation.