IFRS 15: Revenue from customer contracts

The IASB has published IFRS 15 ‘Revenue from Contracts with Customers’ which is effective for annual reporting periods beginning on or after 1 January 2018. IFRS 15:

- replaces IAS 18 ‘Revenue’, IAS 11 ‘Construction Contracts’ and some revenue-related Interpretations

- establishes a new control-based revenue recognition model

- changes the basis for deciding whether revenue is recognised at a point in time or over time

- provides new and more detailed guidance on specific topics

- expands and improves disclosures about revenue.

IFRS 15 will apply to most revenue arrangements, including constructions contracts. Among other things, it changes the criteria for determining whether revenue is recognised at a point in time or over time. IFRS 15 also has more guidance in areas where current IFRSs are lacking – such as multiple element arrangements, variable pricing, rights of return, warranties and licensing.

A single model for revenue recognition

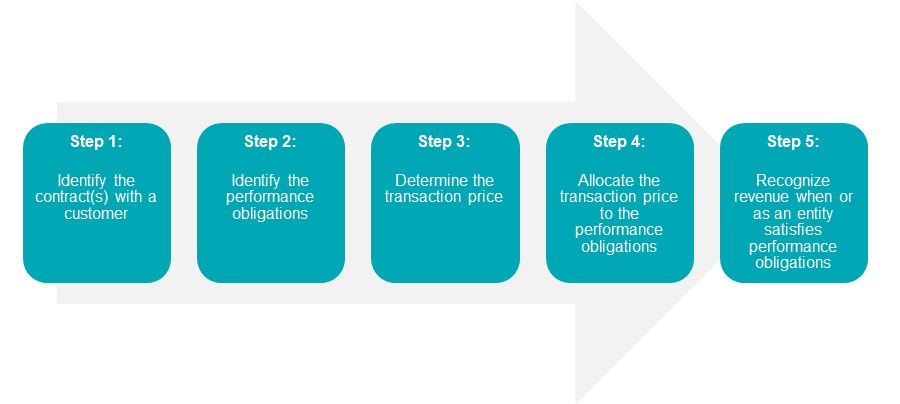

IFRS 15 is based on a core principle that requires an entity to recognise revenue:

- in a manner that depicts the transfer of goods or services to customers

- at an amount that reflects the consideration the entity expects to be entitled to in exchange for those goods or services.

Accordingly, now, there is one single model for revenue recognition in five steps as follows:

Contract modifications

A contract modification arises when the parties approve a change in the scope and/or the price of a contract (i.e. a change order). The accounting for a contract modification depends on whether the modification is deemed to be a separate contract or not. An entity accounts for a modification as a separate contract, if both:

- the scope changes due to the addition of ‘distinct’ goods or services

- the price change reflects the goods’ or services’ stand-alone selling prices under the circumstances of the modified contract.

Besides, IFRS 15 also provided detailed guidance for other topics which were presented in limitation under IAS 18 and IAS 11 such as contract costs, warranties, licensing, rights of return and repurchase obligations, etc.

Presentation and disclosures

Beside revenue arisen from the contract on its statements of profit or loss, IFRS 15 requires the entity to present contracts in its statement of financial position as a contract liability, a contract asset, or a receivable, depending on the relationship between the entity’s performance and the customer’s payment at the reporting date.

IFRS 15 requires to disclose many new information about contracts with customers, including: recongised revenue, contract balances, performance obligations, significant judgements and other related information.

Our full publication on “IFRS 15: Revenue from customer contracts”

For detail instruction on IFRS 15, please read our full report in English at the following link:

Download this newsletter