Taxation in Vietnam – Personal Income Tax (“PIT”)

30 May 2016PERSONAL INCOME TAX (“PIT”)

The new Law on PIT took effect on 1 January 2009. This replaced the previous ordinance and regulations covering Income Tax of High Income Earners in Vietnam.

Individuals liable to PIT and tax resident status

Individuals are subject to Vietnamese PIT upon their tax resident status, i.e. PIT on their worldwide incomes for tax resident or PIT on Vietnam sourced income for tax non-resident.

Any foreign individual shall be considered a PIT resident if he/ she meets one of the following conditions:

- being present in Vietnam for a period of 183 days or more within either a western calendar year or for 12 consecutive months counting from the first arriving date;

- having a permanent residence in Vietnam (including a registered residence which is recorded on the permanent/temporary residence card in case of foreigners);

- having a leased house in Vietnam with a term of 183 days or more in a tax year and unable to prove tax residence in another country

A non-resident is any individual who does not satisfy the above conditions.

Taxable income

Taxable income generally comprises 10 main types of income: employment income, business income, income from capital investments, income from capital transfers, income from real property transfers, winnings or prizes, royalties, income from franchises, income from inheritances and receipts of gifts.

Income not subject to tax generally includes:

Employment

- one-off regional transfer allowances for: (i) foreigners moving to reside in Vietnam, (ii) Vietnamese holding other country nationality working in Vietnam, and (iii)

- Vietnamese working overseas;Once per year home leave round trip airfare for expatriates and Vietnamese working overseas;

- employee training fees paid to training centers;

- school fees up to high school in Vietnam/overseas for children of expatriates/Vietnamese working overseas;

- mid-shift meals (subject to a cap if the meals are paid in cash);

- taxable housing benefit including utilities: being the lower of the actual rental paid and 15 per cent of the employee’s gross taxable income (excluding taxable housing);

- that part of night shift or overtime salary payable that is higher than the day shift or normal working hours salary stipulated by the Labour Code;

- compensation for labour accidents; and

- income of Vietnamese vessel crew members working for foreign shipping companies or Vietnamese international transportation companies

To apply the PIT exemption on the above, there are a range of conditions and restrictions.

Non-Employment

- interest earned on deposits with credit institutions/banks and on life insurance policies;

- retirement pensions paid under the Social Insurance law (or the foreign equivalent);

- income from transfer of properties between various direct family members;

- inheritances/gifts between various direct family members;

- monthly retirement pensions paid under voluntary insurance schemes;

- income from life insurance policies;

- foreign currency remitted by overseas Vietnamese

- scholarships

- compensation payments from life and non-life insurance contracts

PIT deductions

Tax deductions include:

- contributions to mandatory social, health and unemployment insurance schemes;

- contributions to local voluntary pension schemes;Personal and family relief:

- personal relief of VND9 million/month, and family relief of VND3.6 million/month/dependent. The dependent allowance is not automatically granted, and the taxpayer needs to register qualifying dependents and provide supporting documents to the tax authority; and

- contributions to certain approved charities.

PIT administration

- Individual tax code: Any individual present in Vietnam who has taxable income must obtain an individual tax code. Those who have taxable employment income must submit the tax registration file to their employer; the employer will subsequently submit this to the local tax office. For individuals with taxable non-employment income, they must submit their tax registration file directly to the district tax office.

- PIT declaration and payment:

For employment income, Employers must deduct and withhold employees' PIT and submit/ pay it to the tax authority, alongside the relevant social security contributions on monthly basis with the timeline no later than the 20th of following month or on a quarterly basis by the 30th day following the reporting quarter. The total income withheld must be finalized no later than 90 days after the end of the western calendar year.

Expatriate employees are also required to carry out a PIT finalization on termination of their Vietnamese assignments before exiting Vietnam. Tax refunds due to excess tax payments are only available to those who have a tax code.

For non-employment income, the individual is required to declare and pay PIT in relation to each type of taxable non employment income. The PIT regulations require income to be declared and tax paid on a regular basis, often each time income is received.

- PIT credit: For tax residents who have overseas income, any PIT paid in a foreign country is creditable against tax paid in Vietnam subject to certain tax administration procedures.

- PIT year: The Vietnamese tax year is the calendar year. However, in the calendar year of first arrival, his/her first tax year is the 12 month period from the date of arrival. Subsequently, the tax year is the calendar year.

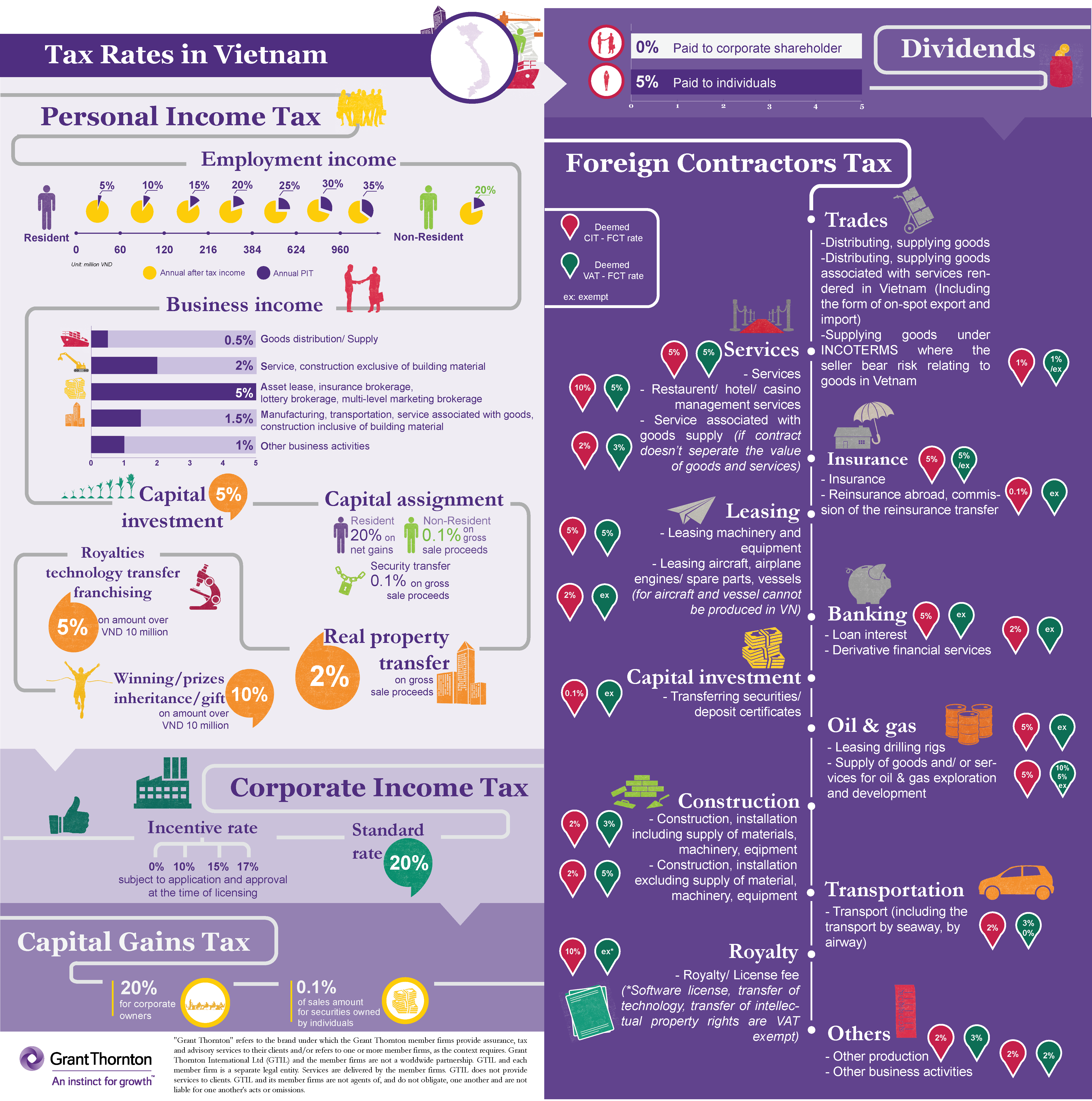

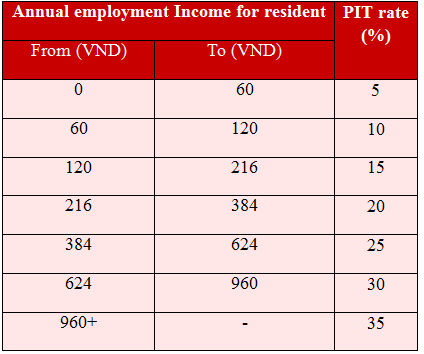

Progressive PIT rates on employment income

Ken Atkinson