Insights into IAS 36

International Accounting Standard No. 36 (IAS 36) ‘Impairment of Assets’ is not a new Standard, and while many of its requirements are familiar, an impairment review of assets (either tangible or intangible) is frequently challenging to apply in practice. This is because IAS 36’s guidance is detailed, prescriptive and complex in some areas.

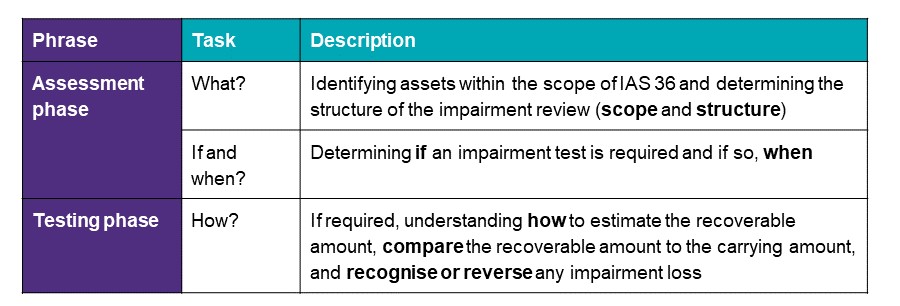

Basically, IAS 36 provides the definition of key terms that are essential to understanding its guidance such as carrying amount, cash-generating unit (CGU), impairment loss, recoverable amount, value in use, etc. Such terms are used in the key principle of IAS 36 – “assets should not be carried above their recoverable amount.”

To accomplish this principle, then, IAS 36 prescribes the procedures that an entity applies to ensure that assets are carried at no more than their recoverable amounts (the impairment review). Very broadly, the impairment review comprises:

- an assessment phase and

- a testing phase, if required.

In which:

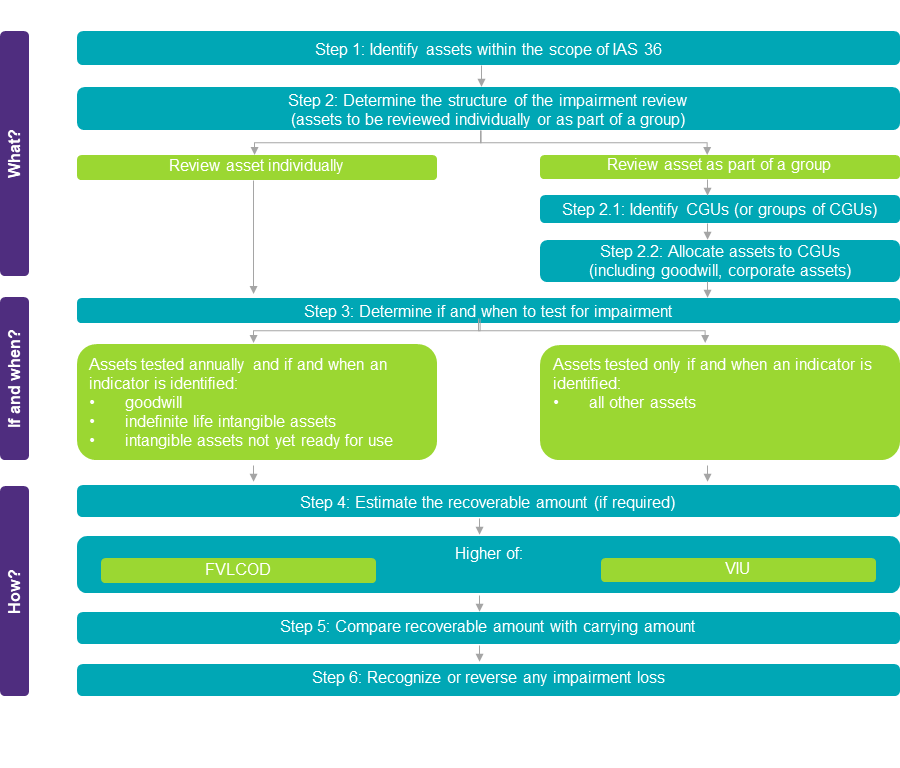

Details of the impairment review in step-by-step are illustrated in the following diagram:

In which:

- FVLCOD represents CGU’s fair value less costs of disposal.

- VIU represents CGU’s value in use which is the present value of the future cash flows expected to be derived from an asset or CGU.

Our full publication on “Insights into IAS 36 – Overview of the Standard”:

For detailed instructions on IAS 36, please read our full report in English at the following link:

Download our newsletter