A finding shows globally business health has declined, in line with the weakening economic outlook

The latest Grant Thornton International Business report findings globally show that overall business health has declined, as expected in line with the weakening economic outlook, with reduced forecasts in economic growth for most, if not all major economies. Nguyen Chi Trung Managing Partner of Grant Thornton Vietnam said “rising interest rates in most developed economies to fight the rising inflation, which is expected to surpass 10% in the UK and USA and some other developed countries, are also driving the global slowdown and reduced economic growth”.

Rising energy costs and falling optimism are the most notable trends in the survey for the H1 2022, Rising energy costs and wage increases are feeding through to higher selling prices however most respondents to the survey are protecting margins by increasing selling prices in line with cost increase or increasing prices more that the increase in costs, meaning that profit expectations remain strong against a backdrop of weakening global trade.

In spite of the weakening global trade many of the respondents to the survey retain strong export expectations for their businesses.

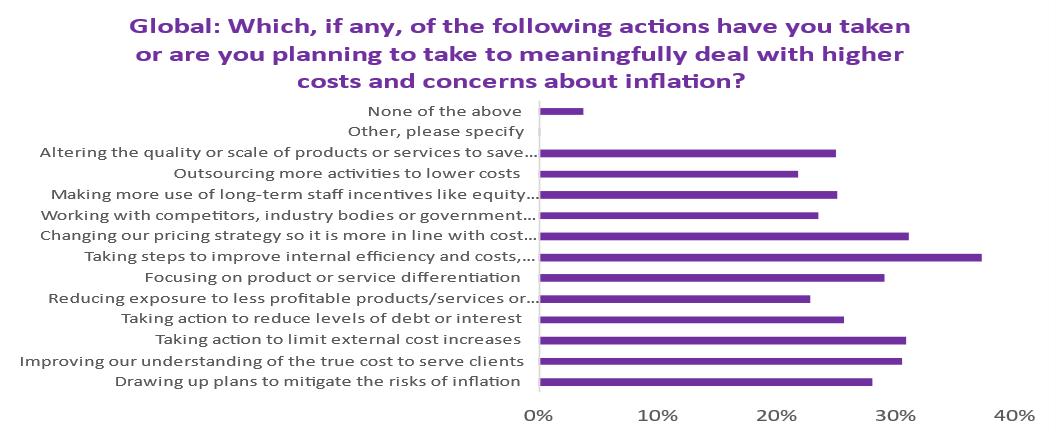

When asked what actions have been taken or are planned to meaningfully deal with higher costs and concerns about inflation the most common answer from approximately 40% of respondents was “taking steps to improve internal efficiency and costs”. The second highest response was changing pricing strategy to be more in line with costs.

Optimism prevailed in Vietnam gaining the number 1 spot globally across 28 countries surveyed with 88% of respondents being slightly or very optimistic, 12 percentage points higher than Indonesia, which ranked number 2 in ASEAN. The percentage for Vietnam was 8 percentage points higher than H2 2021. This is no doubt helped by the current indicators which show that Vietnam should maintain inflation at under 4% projected GDP growth of 7% or more, continued export growth in spite of headwinds) and continued growth in FDI.

Vietnam also gained top spot in expectations for exports with 80% of respondents forecasting a growth, up 15 percentage points from h2 2021. There was also another first when asked about profitability with Vietnam leading the rankings with 87% of respondents forecasting an increase in profits in 2022.

In spite of the optimism 71% of respondents expressed slight or major concern about inflation impacting raw material or other operating costs. However, it seems that they are expecting to be able to pass these additional costs onto customers.

When asked about the impact of the Russia – Ukraine situation 46% of Vietnamese respondents expressed concern that this would lead to higher costs, 44% to supply chain interruption and 35% to loss of new business opportunities.

In response to our specific question for Vietnamese companies as to whether they were implementing ESG policies to better prepare for borrowing and or capital raising the majority of 68% answered in the affirmative, highlighting the importance of this subject now being focused on by lenders and investors.

The final specific question for Vietnamese companies was whether or not they were preparing for a switch from VAS to IFRS in 2025 and 58% replied in the affirmative. Considering the survey is targeted at SME’s this response was very encouraging as it means Vietnamese companies are planning ahead on such issues.

In summary the responses seem to align with the expectations that Vietnam will achieve one of the world’s highest growth rates in 2022 with GDP growth in a range of 7 to 7.5% and a further strong growth in 2023, although this is harder to predict with slowdown expected in some of Vietnam’s major export markets. Vietnam will for sure be able to cap inflation no higher than 4% in 2022 and as Vietnam is net food exporter they are somewhat insulated against food price inflation. Energy prices have been maintained at a constant prices except for petroleum products but these have fallen significantly in recent weeks. New FDI will continue to be a key driver for growth as will the growth of the middle class.

Experts / Authors

-

Kenneth Atkinson OBE With over 42 years emerging market experience and 40 years Asian experience, Ken has undertaken corporate finance transactions in many emerging markets worldwide (Eastern Europe, the People’s Republic of China and several other countries in South East Asia). He has broad experience in advising Clients including commercial banks on project appraisal, debt finance, loan restructuring, corporate restructuring and equity funding.

Kenneth Atkinson OBE With over 42 years emerging market experience and 40 years Asian experience, Ken has undertaken corporate finance transactions in many emerging markets worldwide (Eastern Europe, the People’s Republic of China and several other countries in South East Asia). He has broad experience in advising Clients including commercial banks on project appraisal, debt finance, loan restructuring, corporate restructuring and equity funding.View Profile