Definition of a lease

IFRS 16 represents the first major overhaul of lease accounting in over 30 years. The Standard will affect most companies that report under IFRS and are involved in leasing, and will have a substantial impact on the financial statements of lessees of property and high value equipment.

IFRS 16 changes the definition of a lease and provides guidance on how to apply this new definition. As a result, some contracts that do not contain a lease today will meet the definition of a lease under IFRS 16, and vice versa.

Under IFRS 16 a lease is defined as ‘a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration’.

A contract can be (or contain) a lease only if the underlying asset is ‘identified’. Having the right to control the use of an identified asset means having the right to direct, and obtain all of the economic benefits from, the use of that asset. These rights must be in place for a period of time, which may also be determined by a specified amount of use.

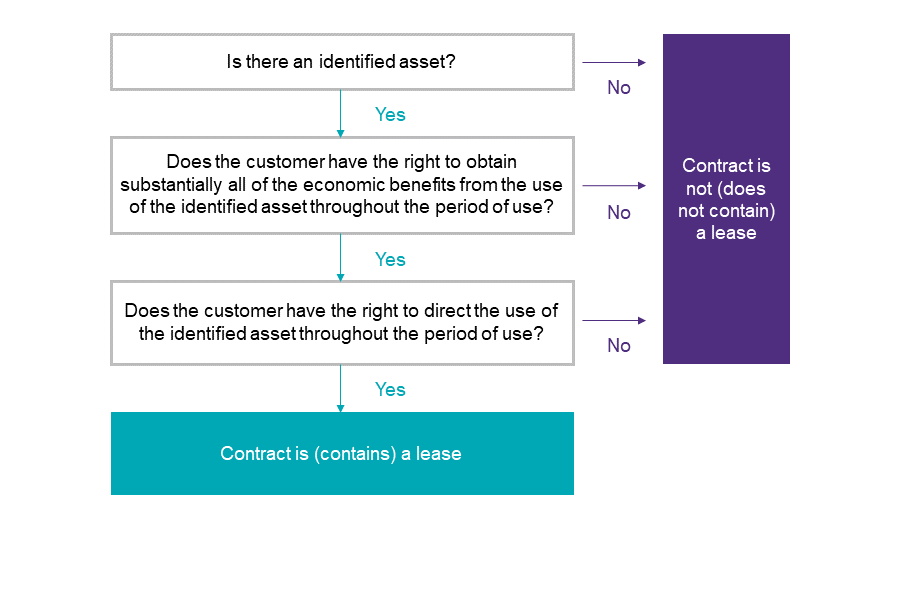

Applying the new definition involves three key evaluations, all of which must be met in order to conclude that a contract is or contains a lease. These evaluations are summarised in the following flowchart:

Is there an identified asset?

An identified asset is an asset that is either:

- explicitly identified in the contract, or

- is implicitly specified by being identified at the time that the asset is made available for use by the customer.

Even if an asset is explicitly specified, a customer does not have the right to use an identified asset if the supplier has a substantive substitution right throughout the period of use.

What is a substantive substitution right?

A substantive substitution right exists if the supplier has the practical ability to substitute alternative assets throughout the period of use and the economic benefits of substituting the asset would exceed the cost (or in other words, the supplier would benefit economically from substituting the asset).

The assessment of whether a supplier’s substitution right is substantive is based on facts and circumstances present at inception of the contract. This means that the customer ignores events that are not likely to occur in future such as:

- an agreement by a future customer to pay an above-market rate for use of the asset

- the introduction of new technology that is not substantially developed at inception of the contract

- a substantial difference between the performance or customer’s use of an asset, and the use or performance considered likely at inception of the contract, and

- a substantial difference between the actual market price of the asset during the period of use, and the market price considered likely at inception of the contract.

Can a portion of an asset be an identified asset?

A portion of an asset is an identified asset if it is physically distinct (e.g. a single floor of an apartment building). Where a portion of an asset is not physically distinct (e.g. 20% of the capacity of an oil pipeline), the portion of the asset is not an identified asset unless it represents substantially all of the capacity of the asset. If neither of these situations exist, the customer is not provided with the right to obtain substantially all the economic benefits from use of the asset and an identified asset does not exist.

Does the customer have the right to obtain substantially all of the economic benefits from the use of the identified asset throughout the period of use?

The second evaluation involves determining whether a customer has the right to obtain substantially all of the economic benefits from use of the identified asset throughout the period of use. There are many ways that a customer can obtain those economic benefits such as by using, holding or sub-leasing the asset.

When making this evaluation, a customer considers its rights within the defined scope of the contract. For example, if a contract specifies that a customer can only print up to a specified number of pages during the period of use of a printer, the customer considers only the economic benefits arising from use of the printer for those pages, and not beyond. Variable lease payments based on the customer’s use of the asset (e.g. variable payments based on sales) do not prevent a customer from obtaining substantially all of the economic benefits from the use of the asset.

Although the customer passes on some of the benefits to the supplier through variable payments, the customer is still the party that receives the economic benefits arising from use of the asset (in this case, the cash flows arising from the sales). IFRS 16 is explicit on this point to eliminate the possibility that companies might include variable lease payments solely to avoid the arrangement being classified as a lease and therefore lease accounting.

Does the customer have the right to direct the use of the identified asset throughout the period of use?

In evaluating whether the customer has the right to direct the use of an identified asset, a customer must have the right to direct ‘how and for what purpose’ the asset is used throughout the period of use. In making this evaluation, a customer considers the decisions that most directly impact the economic benefits to be derived from the use of the asset, including:

- rights to decide the type of output to be produced by the asset(s);

- rights to decide when the output is produced;

- rights to decide where the output is produced; and

- rights to decide whether the output is produced and the quantity thereof.

In many cases, contracts will include terms and conditions that protect the supplier’s interest in the asset, protect its personnel and/or ensure the supplier complies with laws and regulations. These rights are considered to be protective and do not, in isolation, prevent the customer from having the right to direct the use of the asset within the scope of the contract.

Lastly, IFRS 16 is clear that rights to operate or maintain an asset do not give a customer the right to direct how and for what purpose the asset is used, except for when the ‘how and for what purpose’ decisions are predetermined. In this case, the customer will control the asset if the customer has the right to operate the asset throughout the period of use or the customer designed the asset in a way that predetermines how and for what purpose the asset will be used throughout the period of use.

Transition considerations

On transition to IFRS 16, both lessees and lessors can choose whether to apply the new lease definition to all of their contracts or apply transitional relief from reassessing whether contracts in place at the date of initial application are, or contain, a lease. If an entity chooses to apply this relief, then the new lease definition will be applied to contracts entered into or modified on or after the date of initial application (1 January 2019 for calendar year end entities).

Our full publication on “Insights into IFRS 16”

For full information of our insights into IFRS 16, please read our full report in English at the following link:

Download the copy of this newsletter